The political economy of the late twentieth century was marked by a striking juxtaposition. From the mid 1970s an unprecedented peacetime surge in public debt coincided with the liberalization of international capital transactions. In 1970 the debt to GDP ratio of a sample of major OECD countries stood at 40 percent. By the mid 1990s, as an unweighted average, this had doubled to 80 percent. Over the same period the capital account restrictions of Bretton Woods were dropped. Capital moved with a freedom last seen in the 1920s and it moved through financial markets and bank balance sheets with greater capacity than ever before. The combination was explosive. From the 1970s, spooked by large deficits and accelerating inflation, capital markets became jumpy. The chronology of public finances was punctuated by a succession of crises. In 1976 heavy selling in forex and gilt-edged markets forced Britain’s Labour government to accept an IMF program. In 1983 in France the socialist government of François Mitterrand was brought to heel. Not by coincidence 1983 was also the year in which the phrase “bond vigilantes” was coined by the American brokerage house economist Edward Yardeni.

“Bond Investors Are The Economy’s Bond Vigilantes”, Yardeni declared. “So if the fiscal and monetary authorities won’t regulate the economy, the bond investors will. The economy will be run by vigilantes in the credit markets.””[1] As Yardeni later spelled out: “By vigilantes, I mean investors who watch over policies to determine whether they are good or bad for bond investors … If the government enacts policies that seem likely to reignite inflation”, Yardeni elaborated, “the vigilantes can step in to restore law and order to the markets and the economy.”[2]

In fact, as Yardeni coined his phrase, the authorities in all the major advanced economies were restoring control. They did so, not by limiting capital movement, but by following the lead taken by the US Fed with its interest rate hike of October 1979.[3] What became known as the “Volcker shock” and the ensuing high unemployment stopped inflation. It was this spectacular squeeze that set the stage for the “great moderation” of the 1990s. Inflation calmed, but in a world of unrestrained capital mobility, the vigilantes could strike anyone, anywhere at any time. In 1992 Britain and Italy again felt the pressure of currency and bond markets. As Bill Clinton took office in early 1993, the first Democrat to do so in 12 years, there was anxiety on Wall Street that he would overturn the anti-inflation consensus of the 1980s. For Yardeni this was the real “heyday” of the bond vigilantes. The assessment of the LA Times was blunt: “Power will not be held only by the Treasury, the Federal Reserve and Congress. Thousands of bond owners and portfolio managers around the world also will have a collective influence–some economists even say veto power–over the Clinton Administration’s policy choices.”[4] When newspapers reported that Clinton might be considering a significant fiscal stimulus, rates shot up. It was only when Clinton and his team disowned any such plan that bond markets calmed. As Yardeni approvingly remarked: “What is striking is that just a modest uptick in yields got the prompt attention of Clinton and his policy-makers”.[5] Indeed, they did not just get the attention of the Clinton administration, as Bob Woodward chronicled in his highly influential inside report, The Agenda, they changed the direction of the Presidency.[6] The Clinton administration implemented a regime of budget balance and “welfare reform” that more than satisfied the markets. Having climbed from 5.2 percent to just over 8.0 percent between 1993 and 1994, by 1998 10-year Treasury yields eased back to 4 percent. It was against this backdrop that James Carvill, the architect of Clinton’s electoral win, commented in February 1993:[7] “I used to think that if there was reincarnation, I wanted to come back as the president or the pope or as a .400 baseball hitter. But now I would like to come back as the bond market. You can intimidate everybody.”[8]

After the Europeans and the US in the early 1990s, the Asian economies, Russia and then Latin America were next. Between 1997 and 2001 they were convulsed by a series of “twin crises” – capital market and foreign exchange runs – that stretched from Thailand to Argentina. As the new century began, the idea that liberalized capital markets exercised veto power became common sense. In academic economics it was formalized in the notion of the trilemma. Under conditions of capital mobility a country could chose between stabilizing its exchange rate and conducting autonomous economic policy. It could not have both.[9] If that sounded tough, many were convinced that the trade off was, in reality, even more severe. Given that a dramatic slide in currency values in an emerging market was likely to unleash an avalanche of outflows, for most states exchange rate flexibility was not an option. So what governments faced was not in fact a trilemma but a straight-forward and stark choice.[10] One could chose to put on the golden handcuffs of global financial integration, and accept the new consensus of fiscal consolidation and market liberalization, or one could impose exchange and capital controls and retain a degree of economic policy autonomy. In practice there were no takers for the latter option.

In April 2000 Rolf Breuer, the head of the Deutsche Bank, told Die Zeit “politics would ‘more than ever [have to be] formulated with an eye to the financial markets’: ‘If you like, they have taken on an important watchdog role alongside the media, almost as a kind of “fifth estate”.’ In Breuer’s view, it would ‘perhaps not be such a bad thing if politics in the twenty-first century was taken in tow by the financial markets’. For, in the end: Politicians … themselves contributed to the restrictions on action … that have been causing them such pain. Governments and parliaments made excessive use of the instrument of public debt. This entails – as with other debtors – a certain accountability to creditors. … If governments and parliaments are forced today to pay greater heed to the needs and preferences of international financial markets, this too is attributable to the mistakes of the past.”[11] In 2007 former Fed chair Alan Greenspan summed up the wisdom of the new era of globalization. In an interview with the Zürich daily Tages-Anzeiger on 19 September he opined that in the upcoming US Presidential election it mattered little which candidate he supported, since ‘(we) are fortunate that, thanks to globalization, policy decisions in the US have been largely replaced by global market forces. National security aside, it hardly makes any difference who will be the next president. The world is governed by market forces.’[12]

That was in 2007, before the financial crisis hit. The question is how this narrative stands up in the wake of a decade of financial turmoil. Is the image of sovereign debt politics shaped between the 1970s and the early 2000s still plausible?

I

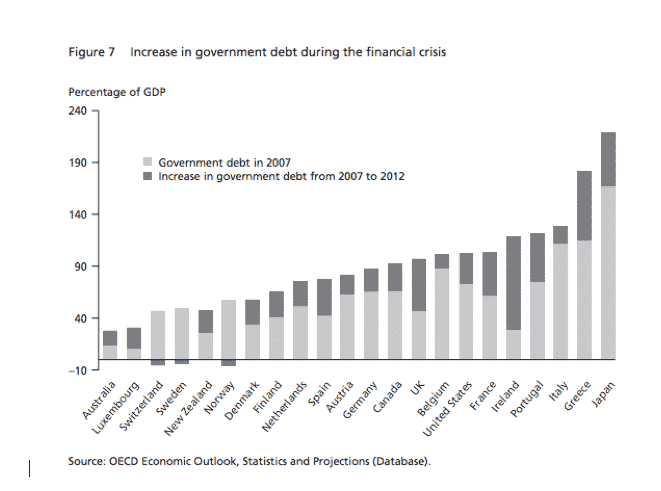

On the face of it, it seems that the crisis must have further tightened the grip of financial markets on politics. The increase in public debt after 2007 was the most dramatic ever seen in peacetime, dwarfing the debt shock of the 1970s and 1980s. In the US alone the increase in Treasury liabilities between 2008 and 2015 came to $ 9 trillion. According to the logic espoused by the likes of Breuer, it is hard to see how this could not have increased the leverage of bond markets.

Source: http://www.mpifg.de/pu/mpifg_dp/dp13-7.pdf

In May 2009 as the scale of the fiscal shock became clear, Bloomberg and the Wall Street Journal reported that markets were up in arms. Yardeni was once more to the fore warning that “Ten trillion dollars over the next 10 years is just an indication that Washington is really out of control ….”[13] On May 29 2009 the WSJ announced that in light of “Washington’s astonishing bet on fiscal and monetary reflation” the bond vigilantes were swinging back into the saddle. “It’s not going too far to say we are watching a showdown between Fed Chairman Ben Bernanke and bond investors, otherwise known as the financial markets.” “When in doubt,” the Journal advised its readers, “bet on the markets.”[14][15] It was a message that had particular resonance inside an Obama administration staffed by veterans of the Clinton years and haunted by memories of the 1990s. In May 2009 Obama commissioned his budget director Peter Orszag to prepare contingency plans for a bond market sell off.[16] Orszag was a protégé of Clinton-era Treasury Secretary Robert Rubin. In the locust years of the Bush Presidency, Orszag had worked with Rubin to craft an agenda of budget consolidation for the next Democratic Presidency.[17]

In early 2010 the appearance of “Growth in a time of debt”, a highly influential paper by Professors Carmen Reinhart and Ken Rogoff, added intellectual weight to fear of the bond market.[18] The two former IMF economists claimed to have identified a critical threshold. When debt reached 90 percent of GDP, growth declined sharply leading to a vicious downward spiral. As Reinhart and Rogoff warned: once debt reached critical levels towards 90 percent of GDP or above, there was always a risk of a sudden shift in market attitudes. “I certainly wouldn’t call this my baseline scenario for the U.S”, Reinhart admitted in one interview – “but the message is: think the unthinkable.”[19][20] On Fox TV historian Niall Ferguson invoked the collapse of the Soviet Russia to make the same point. A world power could be brought down by financial excess with catastrophic speed.[21] Ferguson’s message to American audiences was stark: “The PIIGS R US”.

As the Greek debt crisis went critical in the spring of 2010, debt fear spread around the world. By May 2010 as Alan Blinder put it, the vigilantes were “riled up” and had formed “an electronic mob” circling the globe “faster than Hermes”.[22] The sovereign bond spreads not only for Greece, but Ireland, Portugal, Italy and Spain were all moving upwards. And the tension spilled beyond the Eurozone. The hotly disputed and inconclusive UK election of 6 May 2010 took place in the midst of the most acute early phase of the Eurozone crisis. As British voters cast their ballots, rioting convulsed Athens and the “flash crash” disrupted US financial markets. Not surprisingly, in the aftermath nerves were on edge. Getting Britain’s deficit under control was the central preoccupation of the coalition negotiations.[23] For the Tories and their advisors, it was clear that the budget talks would be “regarded by the financial markets as a test” of their government’s credibility. Market pressure would become the main justification for Britain’s severe austerity course. Even more drastic was the experience of Ireland, Portugal, Italy and Spain, all of which underwent budget tightening enforced by the threat of rising bond yields. In the Geek case, debt restructuring would become a brutal trial of strength. Negotiations stretched for 9 months and resulted in 2012 in a deal that only partially disencumbered the Greek state.[24]

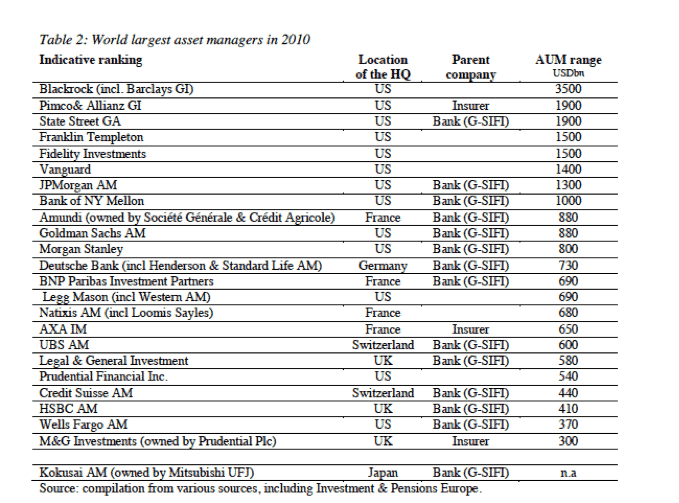

What were the forces, who were the decision-makers moving the bond markets? In the wake of the crisis, this was no longer a question only for market insiders. Campaigning organizations such as the Trade Union Advisory Committee to the OECD and the International Trade Union Confederation began compiling statistics on global asset managers. The sheer size of the capital accumulated by these firms gives an impression of formidable power. The largest of them manage portfolios comparable to the sovereign debt of large European countries.

Source: http://www.ituc-csi.org/IMG/pdf/1203t_bond.pdf

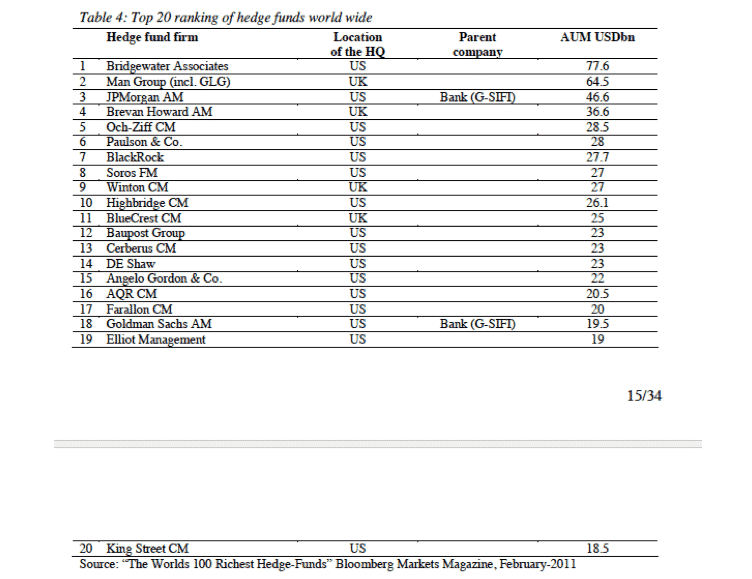

The giant bond funds recalled not so much the vigilantes as the robber baron railway capitalist that displaced them. Truer to the Wild West imagery were the hedge funds. These were far smaller but they were also more aggressive and willing to take risks on massively discounted sovereigns bonds. A handful of so-called “vulture funds” snapping up a few billion dollars worth of devalued debt could exercise huge leverage in complex debt negotiations.

Source: http://www.ituc-csi.org/IMG/pdf/1203t_bond.pdf

And the spokesmen and women of the bond market were not shy about announcing their power. In the spring of 2011 “bond king” Bill Gross of PIMCO gave an interview in which he attacked the deficits of the Federal government in language reminiscent of the Tea Party. Gross told Atlantic magazine: “Sale of Treasury bonds is the easiest way of staging a mini-revolution …”.[25] A Wall Street Journal Op Ed on 23 November 2011 explained: “There is a significant disconnect between the every person has a vote doctrine of representative government and the blunt collective power of money and markets. Most of the time this disconnect is hidden and doesn’t really matter. In times of crisis, as we have seen in Europe, it can become the only thing that matters, overshadowing coalition governments, parliamentary squabbles, constitutional prohibitions and all the rest.”[26] As Kathleen Gaffney who co-managed $ 80 billion in bonds for the Loomis Sayles group, owned by Natixis, put it to the FT, Greece and possibly Portugal would “pay the price for not being harder on the populace”.[27]

Such talk made perfect raw material for a revived interest on the left in political economy. Not surprisingly, the crisis renewed critical approaches to finance and debt.[28] Slavo Žižek, enfant terrible of the radical scene asked rhetorically, “What, then, is the higher force whose authority can suspend the decisions of the democratically elected representatives of the people? As far back as 1998, the answer was provided by Hans Tietmeyer, the then governor of the Deutsche Bundesbank, who praised national governments for preferring “the permanent plebiscite of global markets” to the “plebiscite of the ballot box”.”[29] At a conference hosted by the Soros-funded platform for alternative economic thought, INET, German literary theorist and critic Joseph Vogl remarked: “the markets themselves have become a sort of creditor-god, whose final authority decides the fate of currencies, social systems, public infrastructures, private savings, etc.”[30] The most systematic and influential analysis of public debt from the left was that offered by sociologist Wolfgang Streeck. Indebted capitalist democracies, according to Streeck, face a systematic double bind. They were answerable not just to their citizens, but to a new constituency, the owners of governments bonds. Unlike citizens, credit markets are internationally organized. Their claims are enforceable in law. They have the capacity to exit. The interest rates set by bond auctions “are the ‘public opinion’ of the Marktvolk (AT: market citizenry), expressed in quantitative terms and therefore much more precise and easy to read than the public opinion of the Staatsvolk (AT: state citizenry). Whereas the debt state can expect a duty of loyalty from its citizens, it must in relation to its Marktvolk take care to gain and preserve its confidence, by conscientiously servicing the debt it owes them and making it appear credible that it can and will do so in the future as well.”[31]

Of course, this left critique of capital markets has a pedigree. The idea of bond markets acting as a countervailing force against left-wing governments stretches back at least as far as the early twentieth century when social democratic parties first took the gamble of trying to govern capitalist states. In 1924 the government of the Cartel des Gauches in the French Third Republic was hobbled by what they dubbed the “mur d’argent” (wall of money).[32] In 1931 the British left denounced the “bankers ramp” that split the second Labour government of Ramsay MacDonald’.[33] In the 1940s Polish economist Michael Kalecki theorized about a capital strike.[34] It was an idea that gained further currency as capital flows were liberalized in the 1970s and foreign investors could once again easily withdraw from an economy whose government they did not trust. In 2012 Streeck positioned his Adorno Lectures entitled Buying Time, self-consciously as a revival of crisis theories of the 1970s. The hobbling of Mitterrand’s government by capital market panics in the early 1980s reawakened memories of the 1920s.[35] Thirty years later, the breaking of PASOK in Greece and the Spanish social democratic administration followed a familiar script and the enormous pressure directed against the left-wing governments of Greece and Portugal in 2015 made the rule of capital seem more absolute than ever.[36]

II

The convergence between the cheerleaders of the bond vigilantes on the one hand and the left critics of financial capitalism is striking and by no means accidental. Both have a stake, though from opposite vantage points, in highlighting capital’s watchdog role. What both downplay is the fact that the pressure of bond markets on sovereign borrowers was far from uniform. Capital markets are hierarchically differentiated and power relations between debtors and creditors are more complex than the simple model of creditor dominance would suggest. Investors have to put their money somewhere and they have a deep interest in security. Historically investors have depended on government borrowing to provide them with “safe assets”.[37] As Streeck recognizes “owners of monetary assets appear to depend on safeguarding their portfolios by investing at least part of their capital in government bonds.”[38] If they so choose governments can exert direct control over capital markets. They can engage in what is commonly termed “financial repression” – requiring funds to be allocated to low interest government debt. Furthermore, there is, as Streeck notes, a more elemental risk in lending to sovereigns. “They may also at their discretion one-sidedly ‘restructure’ government debt, since as ‘sovereign’ debtors they are not subject to any legal bankruptcy procedure. …. That is a constant nightmare for lenders.”[39] Indeed, it is with that problem of “original sin” that mainstream, as opposed to critical left-wing accounts begin.[40] Governments as sovereign borrowers have a credibility issue. One solution, historically, has been to give creditors more voice.[41]

Though it is tempting to paint a picture of market dominance over democratic government, the interaction is better described as a never-ending “strategic game”.[42] And the crucial question is, at any given moment, what defines the terms of the game? To offer a more specific answer we need to marry general sociological observations to a systematic international political economy. The pressure the capital markets exercise depends on the position of a state in the global financial hierarchy and the manner of its insertion. Greece, Portugal and Ireland found themselves in the difficulties they did in large part because they were small and tied to the Eurozone. They could not devalue. And even if they had been able to do so, the scale of their debts in a “foreign currency” made the risk of a disruptive avalanche too great. For Latvia in 2009, for instance, a devaluation as recommended by the IMF would have been tantamount to a comprehensive default on its huge euro-denominated debts. Despite the political turmoil it caused, Latvia stayed the course of austerity. Those constraints were not binding on by far the largest sovereign borrower, the US.

As Paul Krugman insisted as far as the US was concerned talk of bond vigilantes was fear-mongering. Not only was the size and the number of the vigilantes exaggerated. But “even if for some reason the vigilantes did attack, it’s very hard to see how they could cause a recession in a country that retains its own currency and doesn’t have large amounts of debt denominated in foreign currency. … a loss of confidence would lead not to a contractionary rise in interest rates but to an expansionary fall in the dollar.’[43] According to Rudiger Dornbusch’s seminal macro model of “exchange rate overshooting”, so long as the central bank held its nerve and was willing to hold short-term interest rates down, the effect of a speculative attack would be to depreciate the currency to the point at which the expected future appreciation provided investors with the rate of return that they needed. In the meantime a lower exchange rate would add to export competitiveness. The vigilantes would be doing their supposed victims “a favor”.[44]

Such qualifications are a salutary corrective to monolithic views of creditor power. But they do not go far enough in addressing the remarkable events we have witnessed since 2008. Whilst on the periphery of the Eurozone, Greece, Ireland, Portugal and Spain enacted a stylized rerun of the clashes of the 1980s, by 2014 global investors were paying Germany to take their money. As Bloomberg reported, contrary to the bond vigilante story line, the crisis led investors to see the bonds of the countries like the US, Germany and the UK as safe havens. The cost of borrowing held steady or fell even as the volume of sovereign debt issued increased spectacularly.[45] Rather than facing a vicious spiral of waning confidence, rising borrowing costs, insolvency and crisis, treasuries and central banks in most of the world seemed to have opened up a virtuous circle in which lower rates made larger debts more affordable. As a result, even as America’s debt surged, its costs of debt service fell from $ 451 bn in 2008 to $ 383 bn in 2009. Even with lower yields and surging volumes of debt issued, the bid-to-cover ratio, which measures the ratio of bids to the quantity of Treasury bonds offered, rose from 2.41 from 2004-8, to 2.63 in 2009 and 3.21 in 2010.[46]

The point of these remarks, of course, is not to erase the extreme victimization of borrowers like Greece. The point, rather, is to throw into stark relief the ideological work done by slogans such as “The PIIGS R US”. Blatant scaremongering helped to maintain the pressure for austerity and to keep borrowing in check even as the terms of borrowing eased. Furthermore, by asking why experience in credit markets was so polarized we are driven to reexamine two assumptions presumed by the familiar narrative of bond market power, but too rarely spelled out. The first concerns the stance of the central bank, the agency that mediates between the state and bond market. The second concerns the underlying condition of the global economy.

III

The most immediate explanation for the extraordinarily easy conditions enjoyed by the largest sovereign borrowers since the onset of the 2008 financial crisis, is the actions of their central banks. The central banks made themselves into purchasers of government on a scale unprecedented in peacetime. The Fed led the way with three consecutive quantitative easing programs, in 2009, 2010 and 2012. The Bank of England was a major buyer in 2009. The Bank of Japan adopted QE on a huge scale in 2013, as did the ECB in 2015. By 2017, according to IMF data, G4 official purchases had absorbed two thirds of the $ 15 bn in new debt issued since 2010.[47] Not surprisingly this scale of official purchases helped to keep bond prices up and yields down.

This contrasted sharply with the conduct of central banks during the “Volcker shock” in the 1980s, when they took the lead in driving up rates. It was this historical experience that became the unspoken assumption of theories of bond market dominance. The central bank was assumed to be passive or even to be taking the side of the bond vigilantes against high-spending governments. To that extent the theories of capital market power were, more or less implicitly, theories also of struggle within the state. Relations between elected governments and capital markets were triangulated by a third pole, the officials, technicians and economists who craft financial and monetary policy. The vast economic policy literature on central bank “independence” is testament to this point.[48] “Independence” in this context means the ability and willingness of central bankers to defy the wishes of elected governments, not their “independence” from the interests or ideas of “the markets”. Though they pursue their careers in Ministries and central banks those officials commonly maintain close relations with the markets and often rotate into positions in the private sector.

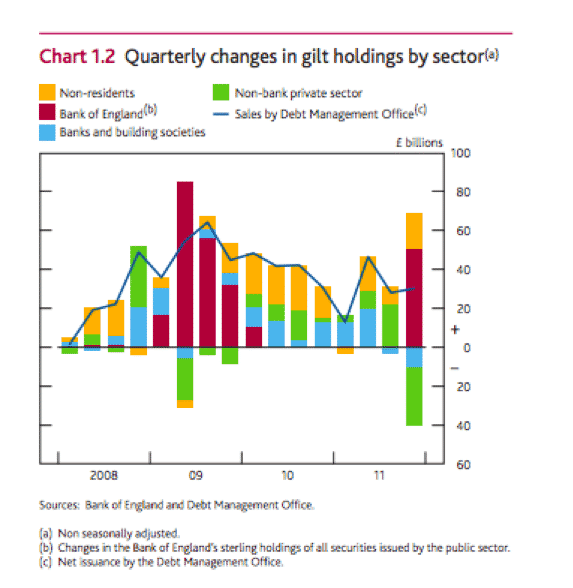

The central bankers of the 21st century were the self-conscious inheritors of this tradition. Notably in Europe they played the role of watchdogs over fiscal policy. Mervyn King of the Bank of England, had no compunction in the spring of 2009 in going on record in Treasury Select Committee to announce: “I do not think we can afford to wait until the Parliament after next before taking action to demonstrate credibly that the United Kingdom is going to reduce its deficit and that fiscal policy will be credible.”[49] And he repeated the message a year later. On May 12 2010 King told the new government: “The most important thing now is for the new government to deal with the challenge of the fiscal deficit. It is the single most pressing problem facing the United Kingdom; it will take a full parliament to deal with . . . I think we’ve seen in the last two weeks, particularly, but in the case of Greece, over the last three months, that it doesn’t make sense to run the risk of an adverse market reaction.”[50] King was acting the role of the central bank enforcer demanding a credible commitment to austerity. But he was playing a delicate game. The central banker needed to vigorously assert his independence also because since 2008 the Bank of England had been propping up the bond market on a massive scale. In 2009 the Bank was overwhelmingly the largest buyer of gilts.

Source: http://www.bankofengland.co.uk/publications/Documents/inflationreport/ir12feb.pdf

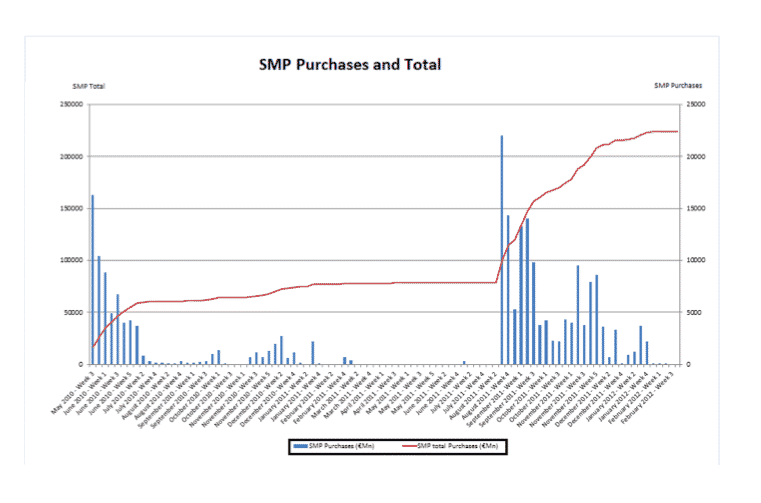

Given the unsettled state of its constitution and the high debt levels in Greece, Italy, Ireland and Portugal, the rules of the “strategic game” played in the Eurozone were rougher. The rhythm of the crisis was set by the cat and mouse game between the ECB, Germany and the lesser players of the Eurozone. The three periods in which tension within the Eurozone built to unbearable levels – November 2009-May 2010, March-August 2011, May –August 2012 – were phases in which the ECB ostentatiously refused to support the public bond market of the common currency zone.

Source: https://placeduluxembourg.wordpress.com/2012/03/02/ecb-market-intervention-the-securities-market-programme-smp/

Jean-Claude Trichet of the ECB made no secret of the fact that he used these tactics to force the slow-moving Eurozone governments to consolidate their budgets.[51] And when that was not enough Europe’s central bankers went further. In Greece, Ireland and Portugal the ECB set the terms of debt negotiations and joined the troika overseeing the program countries. Nor did the ECB confine itself to disciplining the “program countries”. In August 2011 Trichet fired off an extraordinary missive to the Prime Ministers of Spain and Italy demanding retrenchment in the name of sustainability. The letter to Berlusconi was cosigned by Draghi as President of the Bank of Italy and Trichet’s successor at the ECB. The ECB’s threat was that unless the governments acted as the central bank demanded, it would withdraw support both for sovereign and bank debt, allowing the sovereign-bank doom loop to take full effect. Seen from this angle, to talk in terms of “bond market vigilantes” imposing the rules is euphemistic. The role of bond markets in relation to the ECB and the dominant German government was less that of a freewheeling vigilante, than of state-sanctioned para-militaries delivering a punishment beating whilst the police looked on.[52] The question, as with para-militarism in general, was whether the extra-judicial threat once unleashed, could be contained or whether “austerity by fear” would take on a terrifying life of its own. By the summer of 2011 it was increasingly apparent that the strategy of tension had produced something akin to hysteria in the markets. Far from helping to “restore law and order”, the markets for Eurozone sovereign debt were in the grip of a panic. That summer, if the CDS quotations were anything to go by, the probability of default by Italy was judged to be greater than that of Egypt in the grips of the Arab Spring.[53] Three years earlier the same Italian bonds had traded on terms well nigh identical to Bunds.

This lurching adjustment of market judgement, inverted the terms in which the bond vigilante argument was usually cast. Rather than shortsighted governments being disciplined by the “logic of the market”, it was the markets themselves whose rationality was in doubt. Of course, intelligent advocates of markets do not claim that market actors are individually correct in their forecasts or necessarily rational in their individual behavior. The claim is that markets are collectively rational and optimizing. This, however, depends on the operation of checks and balances. So long as the bets by market actors offset each other, speculation will be self-stabilizing. But in a collective panic, even well-judged contrarian bids will be swamped by the general market movement.[54] The vigilantes themselves risk becoming victims of a mob mentality.[55] In the fall of the 2011 it became difficult for cool-headed investors to survive if they had placed bets on the survival of the Eurozone. Not because they were wrong. But because the rest of the market believed they must be wrong.

A case in point is MF Global, the main victim of the huge surge in uncertainty in the fall of 2011.[56] MF Global was a large derivatives broker, headed by the former CEO of Goldman Sachs, that went bankrupt because it had placed a major play not on the collapse but on the survival of the Eurozone. It went bankrupt not because the portfolio of 6.3 billion dollars worth of Eurozone bonds that it had accumulated went into default, but because market anxiety about that bet triggered huge collateral calls. Significantly, once the dust had settled, in December 2011 George Soros spent $ 2 bn snapping up Eurozone bonds being disposed of as part of the MF Global bankruptcy.[57] The difference between MF Global and Soros, was that Soros was operating as a private investor betting his own money and could afford to ignore short-run market sentiment. Most investors don’t enjoy that luxury.

It was the judgement on the part of Mario Draghi and the new management team at the ECB that Eurozone bond markets were too disturbed to any longer exhibit “market logic” that justified their move over the summer of 2012 towards a more proactive position on bond purchasing.[58] It was no longer strictly financial issues that were at stake. The message that Draghi delivered in London in July 2012 was that European politicians had changed the game.[59] Europe was in the process of building a new state structure. If bond markets did not understand this, the ECB would do whatever it took to convince them. In his famous speech Draghi implicitly articulated four essential facts about sovereign bond markets. Modern financial capital is politically and legally constituted. Since its emergence in the 1600s it has been tied to the state and its currency. The Eurozone was adding a new chapter to that history. In moments of stress what mattered were not just durable structures and institutions, but governmental action – the ECB would do what was necessary. Furthermore, its action was generative. The state had the capacity to change the rules of the strategic game as it is played in sovereign debt markets. As Draghi said, the ECB would do “whatever it takes”. And, fourthly, a large state structure – such as the Eurozone has the potential to be – has vast resources at its disposal. Hence the significance of Draghi’s emphatic follow-up: “Believe me! … It will be enough.”

The markets heaved a huge sigh of relief not because they took to heart Draghi’s message about Europe, but because they believed that the ECB was saying that it would in future follow the example of the Fed. It would buy bonds to stabilize sovereign debt markets. Panicking bond markets would no longer be allowed to threaten the fiscal viability of Eurozone sovereigns that were otherwise sound. In fact by the fall of 2012 the Fed was going further than that. When Bernanke launched what became known as QE3 in September 2012 he committed to buying bonds and holding down interest rates until America’s “real” economy recovered. He thus inverted the priorities inherited from the 1970s. Whereas after the Volcker shock, interest rates were sent sky high and the hammer of unemployment was used to bring down inflation, now bond markets would be wrenched out of shape by Fed bond purchases until unemployment fell below 6 percent.

IV

Central bank bond market buying was unprecedented in scale and it was all the more effective because it acted in concert with broader financial forces. Since the late 1990s the balance between sovereign borrowers and investors looking to acquire safe assets had substantially shifted. In the run up to the formation of the Eurozone, many European sovereign borrowers had reduced their debt issuance. The Eurozone’s overall debt to gdp level fell during the early 2000s. At the same time emerging markets and commodity exporters running large current account surpluses were absorbing trillions of dollars of advanced economy sovereign debt.[60] This had the most dramatic impact on the US. Far from facing difficulty in funding the deficits of the Bush years, the one thing that the Fed had difficulty doing from the early 2000s was raising long-term interest rates. The global demand for US Treasuries prevented the Fed’s stepwise increase in short-term rates between 2004 and 2006 from translating into increased long-term rates.[61] This raised fears that the US might at some point face the ultimate bond vigilante attack in the form of a China-lead bond market sell off. But that was not the crisis that transpired in 2007-2008. What collapsed was the market for private label asset-backed securities (ABS).

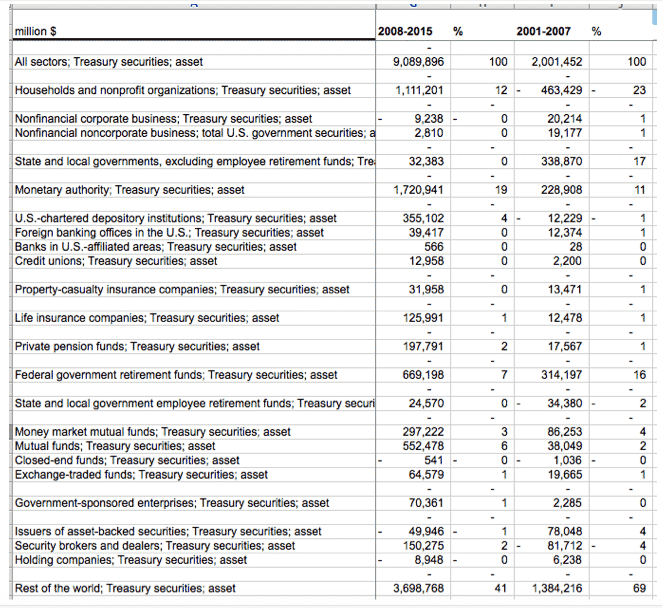

One of the side effects of the shortage of safe assets issued by sovereign debtors from the early 2000s was to create a market niche for financial engineers.[62] This was the essential backdrop to the securitization boom and the spectacular production of private ABS. When that bubble burst the effect was not to unhinge the sovereign debt market, but the opposite. Since trillions of dollars of privately generated securities could no longer be classed as safe assets, government securities offered the only possible alternative.[63] If China had decided to unload its huge holdings of dollar securities in 2008, as Moscow apparently urged it to do, that would certainly have sent an unfriendly signal to Washington. But if the Chinese had been selling they would have found willing buyers. Demand for US Treasuries was strong. The dollar was rising. In fact, China continued to increase its holding of US government debt all the way up to the US government budget crisis of 2011. And as the full extent of the crisis became apparent, the shift from privately generated ABS to sovereign bonds was compounded by the desire of the private sector to deleverage. As households, corporations and banks all tightened their belts, this shift created further demand for safe assets. As a result the $ 9 trillion in new debt issued by the US government between 2008 and 2015 were absorbed at lower interest rates than the US had paid between 2001 and 2007 when issuance came to “only” $ 2 trillion.

US Treasury Securities accumulated 2001-2015

Source: FRB Release Z1

V

If in 2008 the financial crisis drove investors into Treasuries, one might have expected the recovery to induce a reverse shift. Interest rates would gradually rise restoring more normal conditions in capital markets. But that is not what happened. Real rates continued to decline, so much so that in 2013 economists began debating what Larry Summers would dub “secular stagnation”.[64] Growth in GDP and productivity were both declining and long-run real interest rates followed them down, as the return to capital declined. Thus mainstream policy analysts found themselves in surprising agreement with Marxisant political economy in diagnosing a declining vitality of Western capitalism.[65] If as Wolfgang Streeck argues the “ultimate cause” of the public debt build up is “a secular decline in economic growth”, which makes it more and more difficult for governments to satisfy demands for material progress, then that same deterioration in the growth prospects also makes it unprecedentedly easy for governments to attract investors.[66] The lack of profitable private investment opportunities crowds lenders into unexciting but safe public debt.

The surprising upshot was that in an era in which public debt increased more rapidly than ever before, the bond markets lost their bite. In September 2012 Yardeni the original champion of the bond vigilantes, commented despairingly that the Fed’s quantitative easing had made it “next to impossible for vigilantes to ply their trade.”[67] “The bond vigilantes operate in a free market. When you allow them to make judgment calls on what they really want to pay for a bond and what policies are doing and whether those policies suggest that yields should be higher or lower, then the bond vigilantes can do their job. But … (h)ow can there be a market when this massive government entity is intervening to peg interest rates at zero?”[68] At PIMCO there was a similar atmosphere of defeatism. As Bill Gross explained, the mechanics were those of a merry go round. “At 8 a.m., the Fed calls up and asks our Treasuries desk for offers to buy, and one hour later, the Fed’s asking for bids to sell them.”[69]

But are the central bankers really the rulers of the market? Can they dictate terms? The first test of the question would come in 2013 when the Fed decided to test the possibility of ending QE3. In May 2013 Ben Bernanke began discussing the possibility of “tapering”. Then, at 2.15 pm on 19 June 2013, the Fed chair confirmed that bond purchasing might be scaled back from $85 billion to $65 billion at the upcoming September 2013 FOMC meeting, conditional on positive economic news. He also suggested that the bond-buying program could wrap up by mid-2014. The response in the markets was instantaneous and violent. In a matter of seconds yields surged from 2.17 to 2.3 percent. Two days later they had risen to 2.55 percent and would peak at 2.66. These were small changes in absolute terms, but amounted to an increase in borrowing costs of almost 25 percent and inflicted a correspondingly serious capital loss on everyone holding bonds. In the periphery of the world economy the effect was even more dramatic. Emerging market borrowers suffered a savage shock.

If Bernanke had meant to suggest the need for a tightening of monetary policy, his words alone had produced a dramatic and immediate effect. To Richard Fisher, chair of the Dallas Fed and himself a former hedge fund manager, it was reminiscent of one of the great moments of market vigilantism – the 1992 attack on the Bank of England led by George Soros. The markets were testing the Fed’s resolve. Except, that this was the logic of the bond vigilantes in reverse. The Fed was not backsliding on inflation, it was talking tough. The question was whether it had the nerve to carry through. As Fisher put it to the Financial Times in characteristically colorful terms: “Markets tend to test things,” “We haven’t forgotten what happened to the Bank of England. I don’t think anyone can break the Fed … but I do believe that big money does organize itself somewhat like feral hogs. If they detect a weakness or a bad scent, they’ll go after it.”[70] For Fisher it “made sense”, for the Fed “to socialise the idea that quantitative easing is not a one-way street”. But given the likely impact on the fragile recovery of a rapid surge in interest rates he did not expect Bernanke to go from “Wild Turkey to ‘cold turkey’ overnight”. Nevertheless, when the FOMC decided on 18 September 2013 that it “would await more evidence that progress will be sustained before adjusting the pace of its purchases” it came as a shock. The Fed had pulled back. Were the doves on the Fed Board too weak-kneed to impose an interest rate shock? Was monetary policy now dominated by concern to make government borrowing possible? Was it time for the bond vigilantes to ride again? Or was the US economy simply not ready for a tightening? Perhaps it was the Fed testing the markets not the other way around. Given the violence of the market reaction did Bernanke want to demonstrate that neither quantitative easing nor tapering were a one-way bet?[71]

The strategic game between the Treasury, the Fed and the bond markets was dizzyingly reflexive. The result was not a simple power dynamic running in either direction, but a relationship that had about it the air of psychodrama. In October 2014, as the Fed finally steeled itself to end Quantitative Easing, the Financial Times was moved to invoke the box office hit, “Gone Girl”:

““I will practice believing that central banks love me,” is a phrase that may as well have been recited by investors who have tried, for lack of a better alternative, to believe the Fed was their best friend for the past five years. They have been herded into similar positions thanks to years of easy money.

“What are you thinking? What are you feeling? What have we done to each other? What will we do?” – a refrain equally applicable to a concerned policy maker as a nervous husband. The Fed must be eyeing this latest market sell-off very warily.

The whole thing reeks of a marriage built on shaky foundations. Mutual distrust that can lead to a highly combustible situation as investors reassess their historical relationship with unconventional monetary policy at any given time – with deeply unpredictable results.”[72]

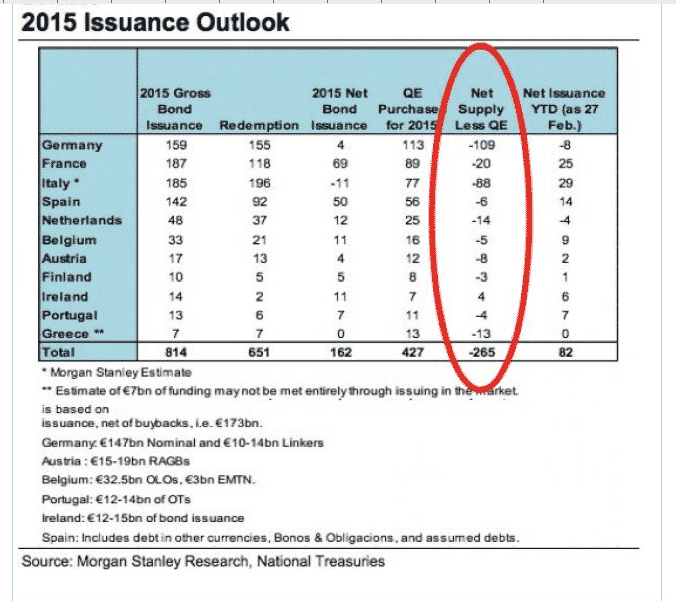

In the event, with the unemployment numbers at satisfactory levels, Janet Yellen, Bernanke’s chosen successor wound up QE on 29 October 2014 without incident. The recovery in the US was anemic, but it was at least firmly established. The same could not be said for the Eurozone. On 22 January 2015 to counter acute fears of deflation the Governing Council of the ECB decided that it would begin buying bonds at the rate of Euro 60 bn per month in a program that still continues at the time of writing.

This had a dramatic impact. It was one thing to operate QE in a situation in which governments were issuing lage quantities of new debt. Those had been the conditions under which QE was first introduced in the US and the UK in 2009 and 2010. By 2015 in the Eurozone the balance was tilted the other way. That year the Eurozone countries were expected to issue only 162 billion euros in new debt. With Draghi’s purchases set to run to 427 billion euro, the net supply of bonds for the Eurozone financial markets in 2015 was expected to be negative 265 billion euro. With Germany issuing barely any new debt the supply of Bunds was squeezed particularly severely.

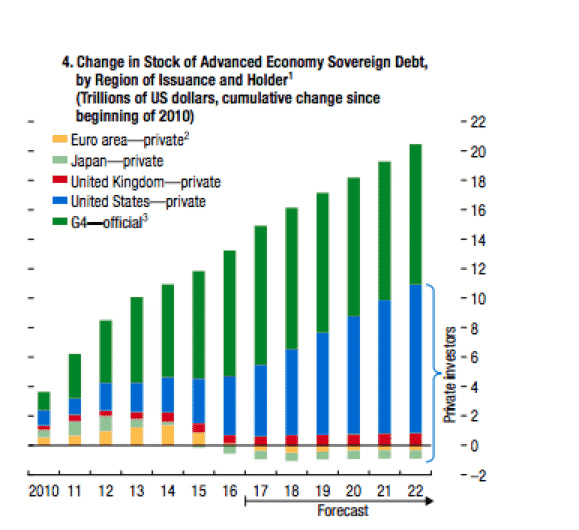

The ECB was not just propping up the market, it was draining it of euro-denominated bonds. In 2017 the IMF published a projection that revealed in stark terms both the reshaping of global public debt markets in the wake of the crisis and their likely future development. It is a picture very different from that which shaped the political economy of sovereign borrowing in the 1970s, 1980s and early 1990s.

Source: IMF Global Financial Stability Report October 2017

Between 2010 and 2012 of the roughly $ 9 trillion issued by the governments of the advanced economies half had been absorbed by central banks. Of the remainder which was placed with private investors, roughly half was issued by the US. By 2017 the balance had dramatically shifted. Of the $ 15 trillion in sovereign debt issued since 2010, two thirds had been absorbed by official purchases, including the entire new issuance of Eurozone and Japanese debt. Virtually all the bonds left for private investors were issued by the US with a small fraction coming from the UK. Over the next five years the IMF predicted that fiscal restraint in Europe and continuing bond purchases by the Bank of Japan and the ECB will tilt the balance further. In effect the US will be the only supplier of highly rated advanced country sovereign debt to world markets. This does not mean that smaller countries will not need to issue small amounts of debt, but whether any of that will be available for global investment will depend on central bank interventions. As far as the large asset managers are concerned, the balance of force between borrowers and lenders has taken on a stark simplicity. The US sovereign debt market watched over by the Treasury and the Fed is the only “strategic game” in town.

[1] http://www.businessinsider.com/bonds-and-nominal-gdp-2013-11?IR=T

[2] http://articles.latimes.com/1992-11-21/news/mn-734_1_bond-market

[3] Helleiner, Eric. States and the reemergence of global finance: from Bretton Woods to the 1990s. Cornell University Press, 1996.

[4] http://articles.latimes.com/1992-11-21/news/mn-734_1_bond-market

[5] http://articles.latimes.com/1992-11-21/news/mn-734_1_bond-market

[6] Woodward, Bob. The Agenda: Inside the Clinton White House. Simon and Schuster, 2007.

[7] http://www.theatlantic.com/magazine/archive/2011/06/the-vigilante/308503/

[8] James Carville political advisor to Clinton Presidency, November 1994. http://content.time.com/time/magazine/article/0,9171,981879,00.html

[9] Eichengreen, Barry J. Globalizing capital: a history of the international monetary system. Princeton University Press, 1998.

[10] Rey, Hélène. Dilemma not trilemma: the global financial cycle and monetary policy independence. No. w21162. National Bureau of Economic Research, 2015.

[11] http://www.zeit.de/2000/18/200018.5._gewalt_.xml

[12] Zürcher Tages-Anzeiger vom 19.09.2007

[13] http://blogs.wsj.com/marketbeat/2008/05/29/return-of-the-bond-market-vigilantes/?mg=id-wsj

[14] http://www.wsj.com/articles/SB124347148949660783

[15] https://www.opendemocracy.net/article/fiscal-expansions-in-submerging-markets-the-case-of-the-usa-and-the-uk

[16] R. Suskind, Confidence Men: Wall Street, Washington and the Education of a President (New York, 2011).

[17] Rubin, Robert E., Peter R. Orszag, and Allen Sinai. “Sustained budget deficits: the risk of financial and fiscal disarray.” AEA-NAEFA Joint Session, Allied Social Science Associations Annual Meetings. 2004.

[18] Reinhart, Carmen M., and Kenneth S. Rogoff. Growth in a Time of Debt. No. w15639. National Bureau of Economic Research, 2010.

[19] http://www.theatlantic.com/magazine/archive/2011/06/the-vigilante/308503/

[20] http://www.theatlantic.com/magazine/archive/2011/06/the-vigilante/308503/

[21] http://www.businessinsider.com/niall-ferguson-sovereign-debt-2010-5?IR=T

[22] http://www.wsj.com/articles/SB10001424052748703315404575250341585092722

[23] https://www.theguardian.com/business/2010/nov/30/mervyn-king-deficit-policy-neutrality

[24] Zettelmeyer, Jeromin, Christoph Trebesch, and Mitu Gulati. “The Greek debt restructuring: an autopsy.” Economic Policy 28.75 (2013): 513-563.

[25] http://www.theatlantic.com/magazine/archive/2011/06/the-vigilante/308503/ and http://www.bloomberg.com/news/articles/2014-12-02/fall-of-the-bond-king-how-gross-lost-empire-as-pimco-cracked

[26] http://blogs.wsj.com/economics/2011/11/23/bond-vigilantes-make-their-votes-known-in-europe/?mg=id-wsj

[27] https://next.ft.com/content/4c0670f6-1c29-11e1-9631-00144feabdc0

[28] See for instance: Bjerg, O. (2014) Making Money: The Philosophy of Crisis Capitalism. London: Verso, Graeber, D. (2011) Debt: The First 5,000 Years. New York: Melville House, Lazzarato, M. (2012) The Making of the Indebted Man. New York: Semiotext(e).

[29] http://www.theguardian.com/commentisfree/2014/jul/13/capital-politics-wikileaks-democracy-market-freedom

[30] https://ineteconomics.org/uploads/papers/Vogl-Paper.pdf

[31] Streeck, Buying Time.

[32] H. Bonin, “Les banques françaises devant l’opinion (des années 1840 aux années 1950)”

[33] For the current state of play on 1931 see Boyce, Robert. “In the Eye of the Storm, May 1931–February 1932.” The Great Interwar Crisis and the Collapse of Globalization. Palgrave Macmillan UK, 2009. 298-344.

[34] Michael Kalecki “Political Aspects of Full Employment”1 [1]Political Quarterly, 1943

[35] Les banques françaises devant l’opinion (des années 1840 aux années 1950) », dans Alya Aglan, Olivier Feiertag et Yannick Marec (dir.), Les Français et l’argent, xixe – xxie siècle : entre fantasmes et réalité, Paris, Presses universitaires de Rennes, coll. « Histoire », 2011, 352 p. (ISBN 978-2-7535-1336-5, présentation en ligne [archive], lire en ligne [archive]), p. 281-302 and Vincent Duchaussoy, « Les socialistes, la Banque de France et le « mur d’argent » (1981-1984) », Vingtième Siècle. Revue d’histoire 2011/2 (n° 110), p. 111-122.

[36] https://www.cambridge.org/core/journals/american-political-science-review/article/structural-dependence-of-the-state-on-capital/34F49B8D6C5D400D62C72C623BD4BF77

[37] Gorton, Gary B., and Guillermo Ordonez. The supply and demand for safe assets. No. w18732. National Bureau of Economic Research, 2013.

[38] Streeck Buying Time.

[39] Streeck Buying Time.

[40] Barry Eichengreen and Ricardo Haussmann (1999), “Exchange Rates and Financial Fragility” Federal Reserve Bank of Kansas City. New Challenges for Monetary Policy pp. 329-368.

[41] North, D. and B. Weingast (1989) “Constitutions and Commitment: The Evolution of Institutions Governing Public Choice in Seventeenth Century England”. Journal of Economic History, 49(4) pp. 803-832 and Bordo, Michael D. Growing up to financial stability. No. w12993. National Bureau of Economic Research, 2007.

[42] http://www.mpifg.de/pu/mpifg_ja/GER_15_2014_Streeck.pdf

[43] http://krugman.blogs.nytimes.com/?s=invisible+bond+vigilantes

[44] http://krugman.blogs.nytimes.com/?s=invisible+bond+vigilantes

[45] http://www.bloomberg.com/news/articles/2010-04-29/where-have-all-the-bond-vigilantes-gone

[46] https://seekingalpha.com/article/3835426-u-s-treasury-auction-showing

[47] IMF, Global Financial Stability Report Octobe 2017. http://www.imf.org/en/Publications/GFSR/Issues/2017/09/27/global-financial-stability-report-october-2017

[48] For a summary see Walsh, Carl E. “Central bank independence.” Monetary Economics. Palgrave Macmillan UK, 2010. 21-26.

[49] Irwin, Neil (2013-04-04). The Alchemists: Three Central Bankers and a World on Fire (pp. 237-238). Penguin Publishing Group. Kindle Edition. https://www.theguardian.com/business/2010/nov/30/mervyn-king-deficit-policy-neutrality

[50] Irwin, Neil (2013-04-04). The Alchemists: Three Central Bankers and a World on Fire (p. 246). Penguin Publishing Group. Kindle Edition.

[51] Bastasin, Saving Europe (Washington DC 2014)

[52] Carlo Bastasin, Saving Europe, Washington DC 2012

[53] Bastasin, Saving Europe, 313

[54] https://next.ft.com/content/c725a322-1287-11df-a611-00144feab49a#axzz1gawCMzGp

[55] Beirne, John, and Marcel Fratzscher. “The pricing of sovereign risk and contagion during the European sovereign debt crisis.” Journal of International Money and Finance 34 (2013): 60-82.

[56] https://www.ft.com/content/138241f6-03dd-11e1-98bc-00144feabdc0

[57] http://www.wsj.com/articles/SB10001424052970204319004577086652040716704

[58] JOURNAL OF LAW AND SOCIETY VOLUME 44, NUMBER 1, MARCH 2017

ISSN: 0263-323X, pp. 79±98 The Bank, the Bond, and the Bail-out: On the Legal Construction of Market Discipline in the Eurozone Harm Schepel*

[59] ECB, ‘Verbatim of the remarks made by Mario Draghi’ 26 July 2012 https://www.ecb.europa.eu/press/key/date/2012/html/sp120726.en.html

[60] G. Gorton, ‘The History and Economics of Safe Assets,’ NBER Working Paper 22210 (April 2016).

[61] B. Bernanke, ‘The Global Saving Glut and the U.S. Current Account Deficit,’ Sandridge Lecture, (10 March 2005).

[62] Bernanke, Ben. “International capital flows and the returns to safe assets in the United States 2003-2007.” Financial Stability Review15 (2011): 13-26 and Caballero, Ricardo J. The” other” imbalance and the financial crisis. No. w15636. National Bureau of Economic Research, 2010.

[63] R.J. Caballero, E. Farhi, and P. Gourinchas, ‘The Safe Assets Shortage Conundrum,’ Journal of Economic Perpectives, 31 (Summer 2017) 29-46.

[64] Summers, Lawrence H. “US economic prospects: Secular stagnation, hysteresis, and the zero lower bound.” Business Economics 49.2 (2014): 65-73.

[65] Magdoff, Fred, and John Bellamy Foster. “Stagnation and financialization: the nature of the contradiction.” Monthly Review 66.1 (2014): 1.

[66] http://www.mpifg.de/pu/mpifg_dp/dp13-7.pdf

[67] https://www.thefinancialist.com/bond-vigilantes-a-factor-in-europe-but-not-in-the-u-s-edward-yardeni/#sthash.3S7zIodh.dpuf

[68] https://www.credit-suisse.com/us/en/articles/articles/news-and-expertise/2012/09/en/bond-vigilantes-get-to-work-in-the-eurozone.html

[69] http://www.theatlantic.com/magazine/archive/2011/06/the-vigilante/308503/ and https://next.ft.com/content/fda5a744-30ec-11e3-b991-00144feab7de

[70] https://next.ft.com/content/9d8fa63e-dce6-11e2-b52b-00144feab7de

[71] http://blogs.reuters.com/anatole-kaletsky/2013/09/19/the-markets-and-bernankes-taper-tantrums/

[72] https://next.ft.com/content/524a2226-55c1-11e4-93b3-00144feab7de