Central bankers everywhere are trying to decide how to respond to the tepid recovery – should they raise interest rates or hold off? In the UK, given political turmoil and Brexit, the decision is particularly difficult, resulting in major ructions at its last rate-setting meeting. See Wren-Lewis’s commentary.

Into this debate steps Andy Haldane, one of the most interesting central bankers around, with a striking speech in Bradford – a classic city of the industrial revolution – on the issue of the labour market and inflation pressures. The headline is that Haldane sounded more hawkish than people expected. But in the process of making his case he offers some interesting analytical material.

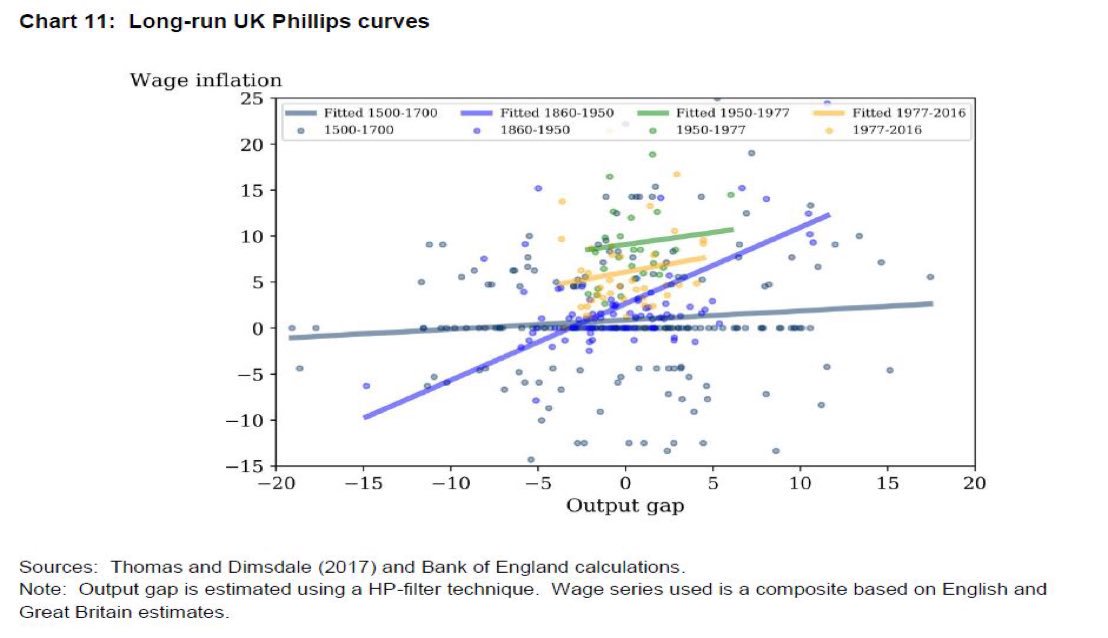

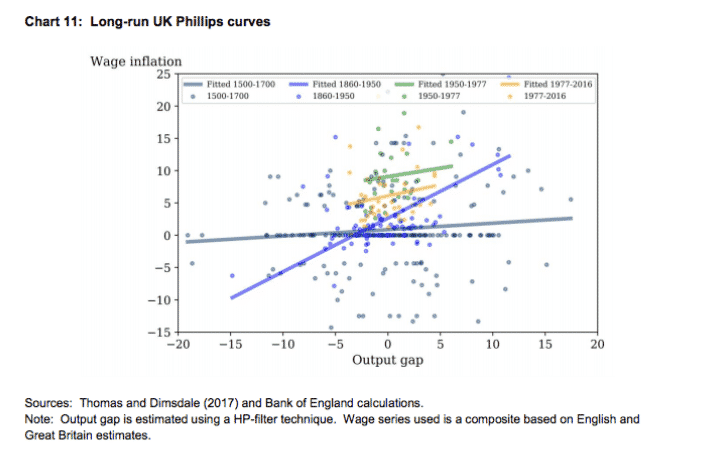

Haldane is an unconventional thinker and likes good charts. The star of his show is a remarkable chart showing the relationship between economic activity (output gap/unemployment) and wage inflation known as the Phillips curve. This is one of the classic charts in macroeconomics. What is new about the Haldane version is the timeline. To place our current post-industrial situation in context the Bank of England has constructed a Phillips curve that maps the entire history of modern capitalism from 1500 onwards.

The result is very striking. There is virtually no positive relationship between economic activity and wages in the Malthusian economy of the period before 1860. Then, as the labour market formalizes, population growth slows down and trade unions organize, a powerful positive relationship between economic activity and wage growth emerges that extends from the 1860s to the 1970s. Since then the relationship has broken down.

This is Haldane’s commentary: “Chart 11 plots UK Phillips curves over three periods: 1500-1700 (pre-Industrial Revolution); 1860-1950 (post-Industrial Revolution); 1950-1977 and 1977 to date (post-war period). In each case, wage inflation is measured on the y-axis and an estimate of the output gap on the x-axis. In the post-war period, the Phillips curve conforms to type. Since 1950, it has a clearly positive slope (less slack in the economy is associated with higher wage inflation) and an intercept which is positive (reflecting positive trend inflation). The Phillips curves covering the periods either side of the Industrial Revolution are more interesting. They share one important similarly and have one important difference. The similarity is that both are associated with an average inflation rate of around zero. This is consistent with the price level being broadly stable over these periods. The striking difference is in the slope of the Phillips curve. The post-Industrial Revolution Phillips curve has a conventional upward slope, similar to that operating after 1950. Higher growth or lower unemployment is associated with higher rates of wage and price inflation. The pre-Industrial Revolution Phillips curve is altogether different; it is as flat as a pancake. Indeed, it bears a close resemblance to the Phillips curves which have operated, in the UK and globally, since 2008. There are many potential explanations of this flatness in the pre-Industrial Revolution Phillips curve, including noisy data. And its similarity with the present-day Phillips curve may be purely coincidental. Nonetheless, this pattern is at least consistent with a shift in working practices, towards a more divisible, idiosyncratic workforce, having contributed to a flatter Phillips curve relationship. None of this evidence is definitive or decisive. Taken together, however, it is at least suggestive that recent trends in the nature of work may have had some bearing both on wage-setting behaviour in general and on the weak wage puzzle in particular. Shifts in working patterns seem very unlikely, by themselves, to have been the prime-mover of weak wages. But they have probably been a contributor in the past and, more significantly, are likely to continue to do so in the future if these trends, as seems likely, perpetuate.”

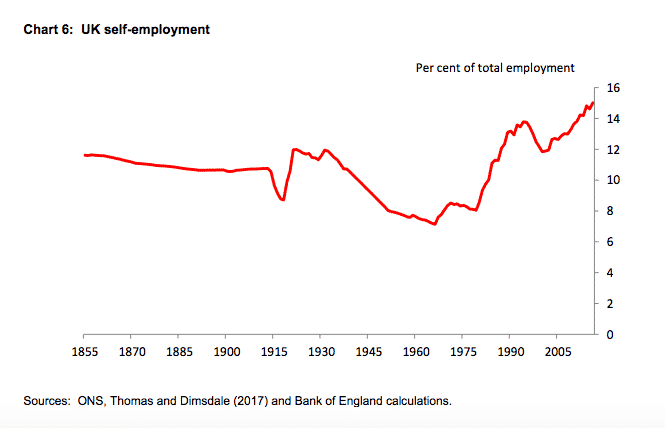

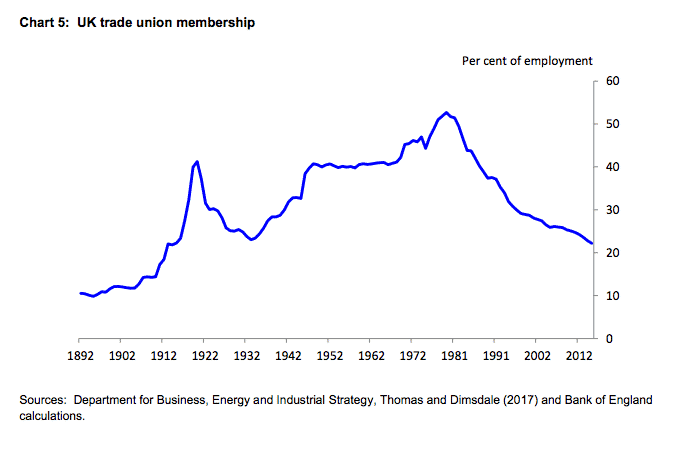

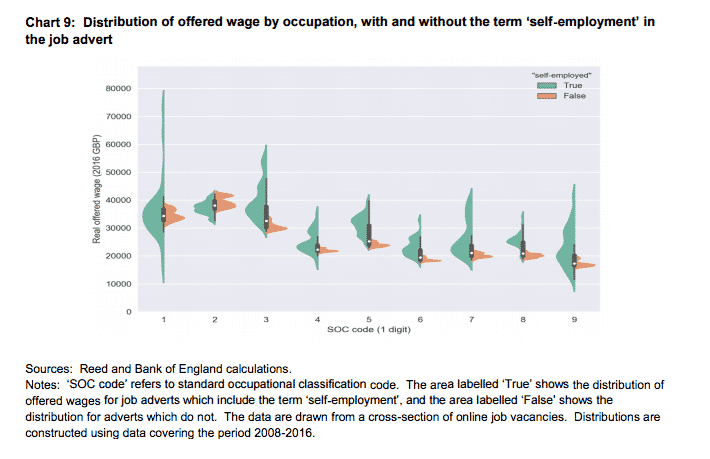

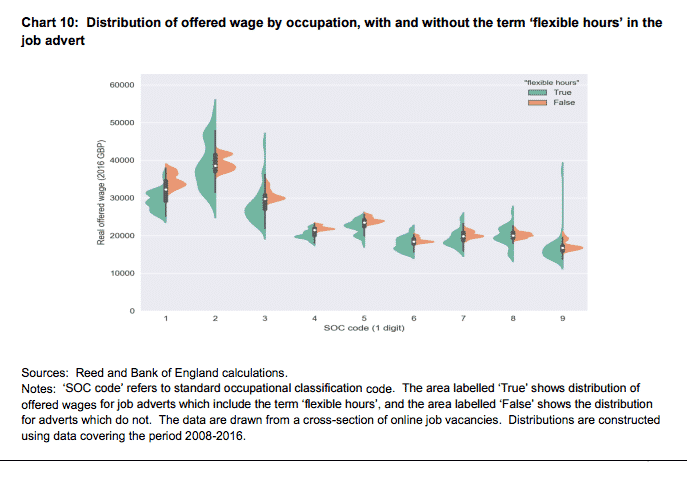

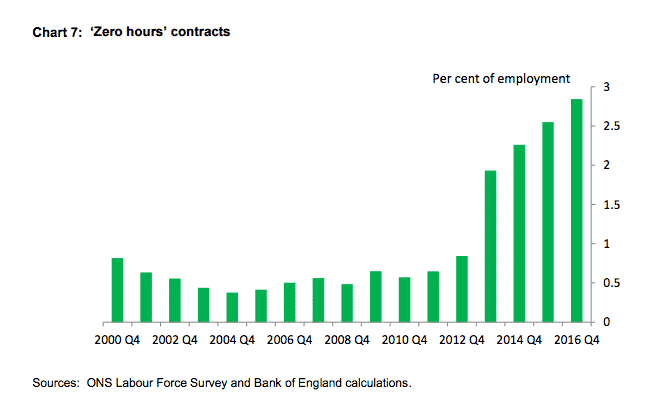

Some other charts from Haldane back up that basic narrative.