Apropos of the Xi Jinping-Trump encounter, there is a fascinating four way conversation going on about Sino-American economic relations between top Western wonks: Larry Summers, Jared Bernstein (ex of the Obama administration, Biden’s chief economist), Martin Wolf of the FT and Brad Stetser (ex-Roubini, CFR, ex Obama, one of the very best economic bloggers).

Everyone agrees that the agenda set by the Trump administration on commercial and currency policy is beside the point. The question is what should be at the center of attention and how great the risks of a Sino-American economic meltdown are.

The chain starts with Summers in full “financial statesman” mode waxing grand strategic about Sino-American economic relations in pages of Washington Post.

“If currency issues are invalid and commercial diplomacy is unlikely to have much positive effect on the U.S. economy, what should be the focus of economic policy with respect to China? It is difficult to overestimate the extent to which China is seeking to project soft power around the world by economic means. Xi’s speech in Davos , Switzerland, in January, quoting Abraham Lincoln and laying out a Chinese vision for the global economic system at a time when the United States is turning inward, was the rhetorical edge of a concerted strategy.

Of course there is Xi’s “One Belt, One Road” initiative, which envisions infrastructure investment and foreign aid to connect China and Europe. In a little-noticed development, the Asian Infrastructure Investment Bank, a Chinese-sponsored competitor to the World Bank, has announced that it will invest all over the world. Already, Chinese investment in Latin America and Africa significantly exceeds that by the United States, the World Bank and relevant regional development banks. And China will soon be the leading exporter of clean energy technologies.

This investment will, over time, secure Chinese access to raw materials, allow Chinese firms to gain economies of scale and help China to win friends. The United States has chosen not to join the Asian infrastructure bank, to undermine rather than lead global cooperation on climate change and, if the president gets his way, to sharply cut back foreign aid. In doing so, it is accelerating a loss of its preeminence in the global competition for prestige and influence. Perhaps this development is inevitable, but it is a mistake to accelerate it.

A truly strategic U.S.-China economic dialogue would revolve around the objectives of global cooperation and the respective roles of the two powers. It is important that such a dialogue start soon, but this move will require the United States to focus less on specific near-term business interests and more on what historians will remember a century from now.”

Jared Bernstein pushes back arguing that it worries him to find Summers in full “poli sci” mode “though he may have an important point”. What worries Bernstein is that there may be serious causes of ECONOMIC tension that may not be amenable to financial statesmanship of the Davos, Kissinger-Summers variety.

And the piquancy is that Bernstein can mobilize Summers against himself: “Larry is surprisingly blasé about a China problem: excess savings (really, an East Asia problem, as Brad Setser points out). I associate this problem with Summers’ own work on “secular stagnation”—persistent demand shortfalls even in recovery. Another way to view sec stag is as a function of excess savings: the globe is awash in more savings that we have good, productive uses for. That, in turn, can lead to depressed interest rates, credit bubbles, large trade surpluses in savings glut countries, which in turn force large trade deficits elsewhere, and high unemployment, depending on what offsets are in play in trade deficit countries. Larry himself has recognized this problem (as has Ben Bernanke since the mid-2000s in his seminal savings glut speech) and wisely called for public infrastructure investment to help offset it.

Our trade deficit with China is 1.6 percent of GDP; that’s a significant drag on demand. In terms of offsets, the Fed is pushing in the other direction (tightening) and the fiscal authorities…um…Congress…can’t find the light switch. We’re of course doing better than most other advanced economies, but here we are in year eight of an expansion and (slight) output gaps still persist.

Interestingly, a smart paper by Larry et al. provides an explicit role for such capital flows in dampening demand and making it harder for the US to hit higher growth rates (“We find capital flows transmit recessions in a world with low interest rates and that policies that trigger current account surpluses are beggar-thy-neighbor.”)

Apart from Summers own technical NBER paper Bernstein also references a really outstanding piece by Martin Wolf in the FT on precisely the issue of what is really at stake in the Sino-American relationship. I’m going to quote liberally but this kind of thing is really why it is worth paying for access to the FT.

Wolf: “US policymakers should worry about China’s capital account, not its current account. That is where danger now lies. Why does the capital account matter more? The answer is that this is where two interrelated aspects of an economy interact with the world economy: macroeconomic balances between savings and investment; and the financial system. In both respects, the Chinese economy is, to cite the celebrated words of former premier Wen Jiabao, “unstable, unbalanced, uncoordinated and unsustainable”. That was true in 2007, when he said it. It is truer today. As the Chinese authorities realise, but their western counterparts may not, the integration of China’s financial system into the global economy is fraught with peril.”

What Wolf is going to deliver, unremarked by Bernstein, is precisely the synthesis of concerns about grand strategic management AND macroeconomics that get split between the two Americans. I’m NOT a Wolf fan-boy. But the difference here is really telling.

Wolf goes on: “Annual gross savings in the Chinese economy amount to 75 per cent of the sum of US and EU savings, at over $5tn last year. China’s gross investment, at 43 per cent of gross domestic product in 2015, was still above its share in 2008, even though the economy’s rate of growth had fallen by at least a third. To sustain such high investment, the ratio of credit to GDP soared from 141 per cent of GDP at the end of 2008 to 260 per cent at the end of last year. The “shadow banking system”, in the form of “wealth management products” and other instruments, has exploded. Interbank lending has also soared. Last, but not least, the banking system is now the world’s largest. Financially, China is the wild east. Remember what the wild west did over the last century: the Great Depression and Great Recession originated in the interaction between US-led finance and the global economy. In view of its macroeconomic imbalances and financial excesses, China could deliver at least as much global financial mayhem.”

Compared to its remarkable 43 % investment rate, “In 2015, gross national savings were 48 per cent of GDP. World Bank data show that households contributed only a half of this. The rest came from corporate profits and government savings (AT a very interesting point to follow up on). International comparisons suggest that economic growth of 6 per cent warrants investment of little more than a third of GDP. This indicates that China’s surplus savings — surplus, that is, to domestic requirements — may be as much as 15 per cent of GDP.”

Why does all this matter for Sino-American relations and the world economy generally?

“Where might such surpluses go? The answer is abroad, in the form of current account surpluses. That is what happened before the financial crisis. It is likely that this is what would also happen now if the government relaxed exchange controls and brought credit and debt growth to a halt. Capital would pour out, the renminbi would tumble and, in time, a globally unmanageable current account surplus would emerge.”

So this is the new disaster scenario. The dikes break in China and we see a sudden domestic implosion and a huge correction in the balance of payments that ripples out across the world economy. This time it would not be an official build up of dollar reserves but a gigantic flow of private funds that would drive the exchange rate down and produce a huge trade surplus. As Setser puts it “The resulting outflow of private funds would push China’s exchange rate down, and give rise to a big current account surplus—even if the vector moving China’s savings onto global markets wasn’t China’s state. History rhymes rather than repeating.”

So, is it better that China should maintain its controls? Well, yes. But that has risks too. Wolf:

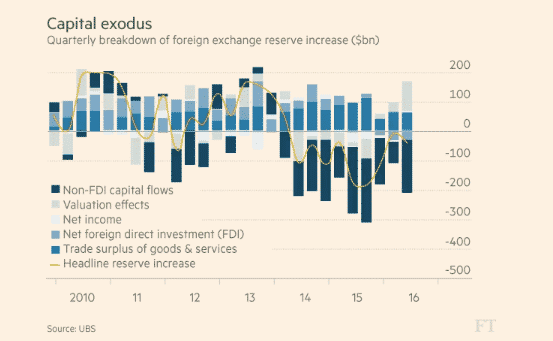

“Today’s credit growth and consequent financial fragility are a direct consequence of the desire to prevent this from happening. It has been the way to keep investment up at uneconomic levels. The Chinese authorities are in a trap: either halt credit growth, let investment shrink and generate a recession at home, a huge trade surplus (or both); or keep credit and investment growing, but tighten controls on capital outflows. … Why is the latter essential? With such large and growing stocks of liquid, risky or low-yielding financial assets, plus a huge flow of savings, not to mention the anxieties caused by the anti- corruption campaign, Chinese corporations and individuals have been desperate to take money out. This explains why, despite a persistent trade surplus, the country’s foreign exchange reserves fell from $4tn in June 2014 to $3tn in January 2017.”

Is there any way out? Market fundamentalists might be tempted to argue for shock therapy. The idea would be that there is unsatisfied demand for cross-border flows in both directions. There are Chinese would want to get their money out, but non-Chinese would want to invest their money in China. See the FDI discussion of my previous post. Those flows might cancel out, so we could float free of controls without overall disturbance.

Wolf is skeptical: “Suppose the Chinese authorities adopted, instead, the alternative policy of rapid liberalisation of both inflows and outflows, while relying on credit expansion to sustain domestic demand. It is possible, but unlikely, that the flow of money into China from abroad would match the outflow, as foreigners and Chinese both diversified their portfolios. Yet that would also cause three headaches. First, the domestic macroeconomic imbalances would persist. Second, the financial sector would become still more fragile. Finally, this vast, complex and fragile financial system would become fully integrated with the rest of the world’s, itself still far from fully stable. Instead of the Chinese financial crisis that many now think imminent, this would enormously increase the likelihood of another global crisis with China, not the US, at its heart.”

And then Wolf twists back one again to the geopolitical punchline: “These are huge challenges that need to be discussed in full between the US and China (and others). They have profound implications for trade, but they are not about trade policy at all. They require joint consideration of macroeconomic and financial policy. They also demand attention to the management of China’s external account: above all, exchange controls, the exchange rate and foreign currency reserves. Mr Xi has people in his government who at least understand these issues. Is the same also true for Mr Trump? The stability of the world economy depends on the answer. Alas, I suspect it is no.”

Wolf’s outstanding post elicited an intervention by Brad Setser at the CFR, which adds a further fascinating dimension. Setser does not deny the basic Wolfian diagnosis, but mines the Chinese balance of payments data to asses what instruments of control might be at Beijing’s disposal.

Setser: “I suspect that China’s regime was under less outflow pressure in 2016 than implied by the (large) fall in reserves, and thus there is more scope for a combination of “credit and controls” (Wolf: “The Chinese authorities are in a trap: either halt credit growth, let investment shrink and generate a recession at home, a huge trade surplus (or both); or keep credit and investment growing, but tighten controls on capital outflows”) to buy China a bit of time. Time it needs to use on reforms to bring down China’s high savings rate.”

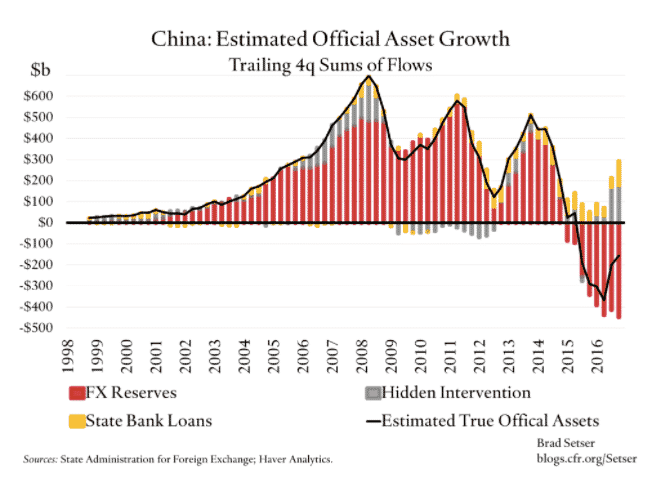

Setser arrives at this conclusion by the kind of breakdown of balance of payments numbers, which he does better than anyone and must have made him a formidable contributor at Treasury. The question is who actually controls the funds that are leaving China. Are they the fear driven exodus of investors worried about (a) a market crash or (b) the anti-corruption drive? Or is it something else?

Setser: “All close observers of China know that China has been selling large quantities of reserves over the last 6 or so quarters. The balance of payments data shows a roughly $450 billion loss of reserves in 2016, with significant pressure in q1, q3, and q4. The annualized pace of reserve loss for those three quarters was over $600 billion (q2 was quite calm by contrast).

But close examination of the balance of payments indicates that Chinese state actors and other heavily regulated institutions were building up assets abroad even as the PBOC was selling its reserves. In other words, a lot of foreign assets moved from one part of China’s state to another, without ever leaving the state sector.

For a some time I have tracked the balance of payments categories dominated by China’s state—and, not coincidentally, categories that experienced rapid growth back in the days when China was trying to hide the true scale of its intervention. One category maps to the foreign assets the state banks hold as part of their regulatory reserve requirement on their deposit base. Another captures the build up of portfolio assets (foreign stocks and bonds) abroad, as most Chinese purchases of foreign debt and equity historically has stemmed from state institutions (the state banks, the CIC, the national pension fund). Even if that isn’t totally true now, portfolio outflow continues to take place through pipes the government controls and regulates.

These “shadow reserves” rose by over $170 billion in 2016, according to the balance of payments data. The state banks rebuild their foreign currency reserves after depleting them in 2015, and there were large Chinese purchases of both foreign equities and foreign debt.

And the overseas loans of Chinese state banks—an outflow that I suspect China could control if it wanted to—rose by $110 billion.”

As a result much of the foreign exchange that the central bank sold ended up in the hands of other state actors. My broadest measure of true official outflows* shows only $150 billion in net official sales of foreign assets in 2016.

“ That kind of outflow can easily be financed out of China’s large foreign exchange reserves for a time, or China could more or less bring the financial account into balance by limiting the buildup of foreign assets by the state banks and simultaneously cracking down on outward FDI (over $200 billion in outflows 2016, and largely from state and state-connected companies).

In other words, much of the reserve draw was offset by the buildup of other state assets—especially counting the assets state banks and state firms acquired abroad.**

That I suspect is why flows suddenly started to balance once China tightened its controls (and likely made it harder for one part of the state to bet against another part of the state). Of course, the renminbi’s relative stability against the dollar also helped—you do earn more on a bank deposit in renminbi than on a bank deposit in dollars.”

General questions about hegemonic leadership (Summers) –> reminders about macroeconomics (Bernstein) –> links between macroeconomics and finance and back to questions about managerial capacity (Wolf) –> in-depth accounting of link between macroeconomic accounts and managerial structure (Setser) … I’d call that a dialectical progression!

But the upshot remains the same: we have a lot riding on Beijing!