The surge in Chinese FDI in the US in 2016 was remarkable:

https://qz.com/876693/chinese-investment-in-the-us-skyrocketed-in-2016/

Combined with Xi Jinping’s visit, this triggered a flurry of recent reports about Chinese investment activity in the US and the tensions this may cause with the Trump administration. See the FT, WSJ, Bloomberg I, Bloomberg II, Skadden, Reuters, LA Times.

Though this is no doubt about the disruptive impact of the new President, this surge of concern about Sino-American relations around FDI has a striking parallel in similar stories in Germany from the fall of 2016. In Germany the debate circulated around the attempted Chinese takeover of a chipmaker, which in a highly unusual move were blocked by German authorities (at American prompting), and heated exchanges between Berlin and Beijing during a visit to China by Sigmar Gabriel (SPD) then Minister for Economic Affairs.

First key takeaway: Trump’s an economic nationalist and tensions with China are likely to mount, but this is not a phenomenon limited to the US and its terrible new administration. These tensions are classic expressions of new dynamic of uneven and combined development unleashed by China’s astonishing growth.

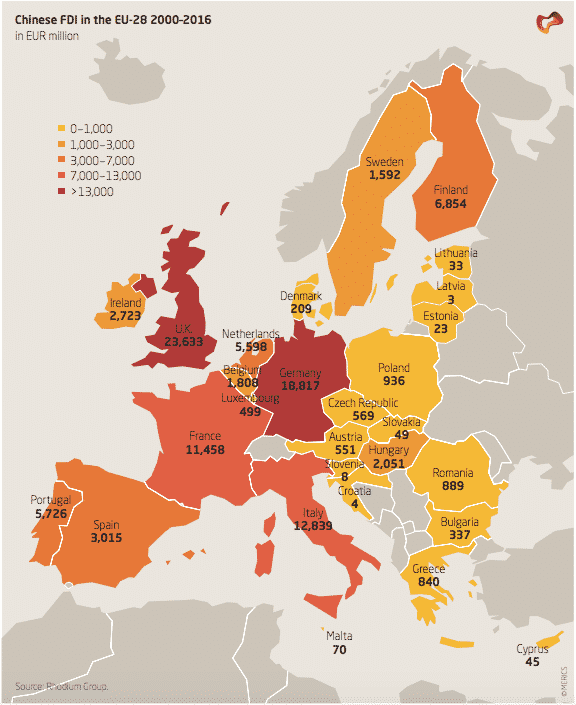

The basic driver is the scale of China’s FDI surge. This is big and likely to get bigger. At least part of this FDI surge is linked to concerted industrial strategy on the part of Beijing. This creates considerable tensions in both Europe and the US and between them. It reveals fundamental asymmetries in international economic interactions which become increasingly difficult to live with as China becomes one of the major hubs of world trade. By the fall of 2016 China was Germany’s major trading partner outside the EU. 2016 was also the year in which Chinese FDI to Germany overtook German FDI in China.

As Gapper comments in the FT: “WTO accession was intended to bring global companies more access to China, and did so in sectors such as carmaking.” As everyone in Germany knows China is now essential to the future of VW, as it is to GM. The competition between the two in China is furious. As Gapper continues, despite allowing some key foreign investments, “China maintains a plethora of formal and informal limits on foreign ownership in healthcare, logistics, telecoms and other industries. China Oceanwide was free this week to buy Genworth Financial, a US insurer, for about $2.7bn, but overseas insurers still have only a tiny market share in China. Ownership limits had a legitimate purpose: to prevent China’s industries being trampled in a stampede of inward investment. But its rapid economic advance in the past 15 years has not led to much liberalisation: even when laws are relaxed, provincial governments and local officials favour Chinese companies in myriad ways. Germany is in a tough spot, lacking any broad mechanism to control China’s advance: the EU has no equivalent of the Committee on Foreign Investment in the US, which investigates sensitive takeovers. The EU has pressed China to allow European companies easier entry but Beijing is a hard bargainer and the imbalance suits it well.”

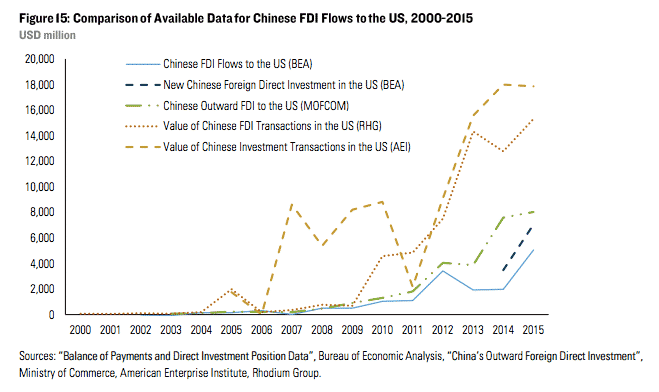

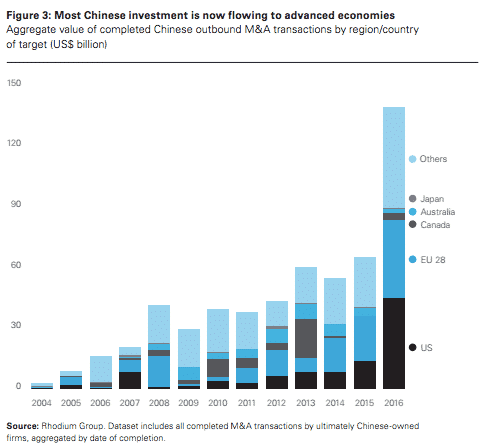

The scale of the Chinese foreign investment surge is dramatic. China has moved from being a net importer to a net exporter of FDI. After the US in 2016 China was the second largest source of M&A in the global economy. It has diversified the location of its investments from a heavy focus on developing and emerging markets to rich countries, first Europe, now the US as well.

The overwhelming majority of Chinese FDI is by private companies and it consists largely of M&A activity rather than greenfield investment. Key deal brokers are Chinese nationals who formerly worked for Western investment banks. AGIC, the firm that brokered the Krauss Maffei, is a private investment fund headed by Henry Cai ex of Deutsche Bank.

Much of the investment is driven simply by ordinary profit seeking commercial behavior. It is not easy to track and there are telling divergences between relatively coarse national economic data and more specialized databases built up by private think tanks and other monitors.

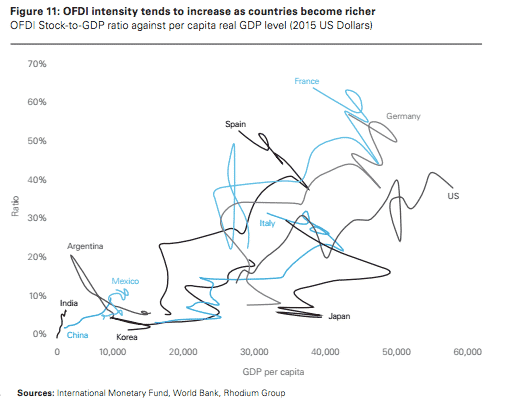

The trend should not be surprising, economist point to a historical regularity whereby the net balance of FDI shifts from the import of capital to the export of capital when countries reach ca. $ 15,000 in PPP adjusted modern dollars.

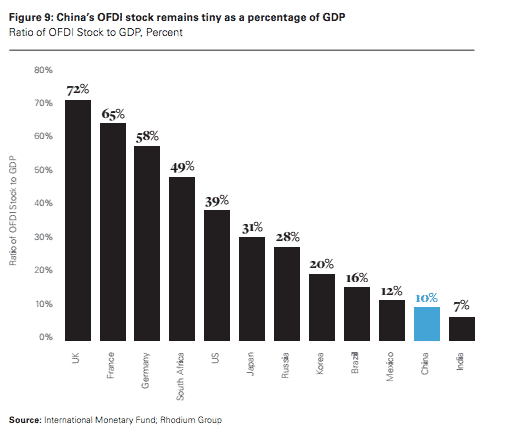

China’s FDI intensity is still very low and will likely increase with time, barring disasters (see below).

At the same time, however, one of the features of Chinese investment that provokes tension is that some of it is clearly strategically directed.

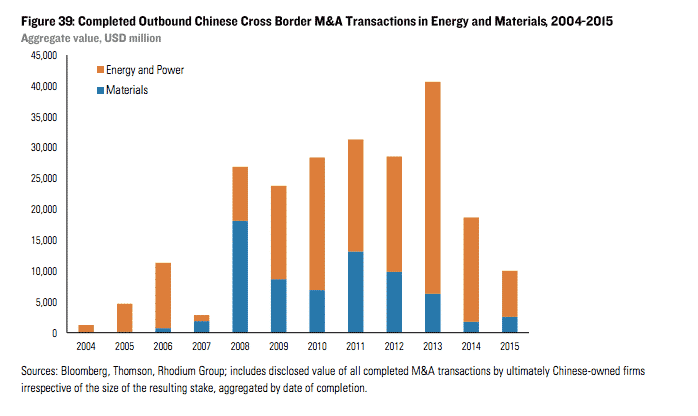

The first wave of reportage about Chinese FDI focused on its investments in energy and raw materials. Under the slogan “going out”, tens of billions were sunk into securing key inputs to the Chinese economy.

As the Rhodium group comments: “From 2005 to 2013, Chinese companies spent US$198 billion on global acquisitions in energy and basic materials assets, accounting for 67 percent of China’s total outbound M&A value in that period. … Chinese acquisitions mostly targeted resource-rich economies in the Middle East, Central Asia, Africa and Latin America. As Chinese investors gained appreciation for political risk and the unconventional oil and gas boom opened up new opportunities, investment shifted to politically stable, resource-rich countries such as Canada, Australia and the US. From 2008 to 2013, those three economies accounted for almost half of total Chinese outbound M&A.”

Under the Made in China 2025 program launched in 2015 China is trying to address the risks of the so-called “middle income trap” by focusing on technological upgrades to its manufacturing base. http://english.gov.cn/2016special/madeinchina2025/

This entails shifting the geographic focus of FDI to advanced economies.

In Europe, Chinese investment is increasingly focused on rich and large economies rather than cherrypicking bargains in bankrupt Greece.

Whereas in the first phase of opening it acquired technology through more or less “voluntary” transfers from foreign firms doing business in China – most notoriously the “transfer” of high speed rail technology from Siemens, Alstom and Kawasaki – it now seeks to build its technology base through foreign acquisitions.

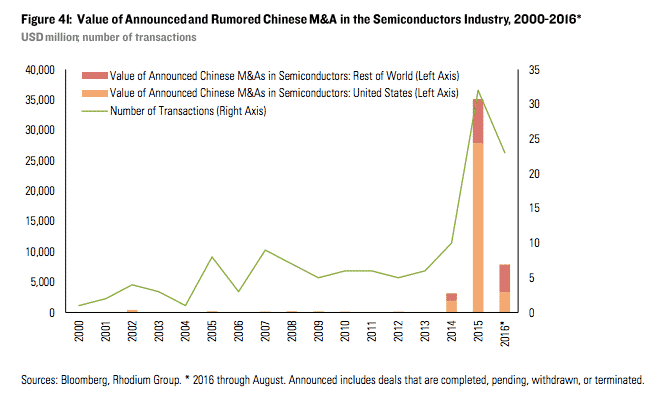

A particularly pronounced instance is the microchip business. In 2015 China accounted for 29 % of global demand for chips, largely imported. Since 2013 it has been pursuing a policy to become more self-sufficient. From $ 1 bn in MA deals per annum the total surged to $ 35 bn in bids in 2015. The National IC fund and Tsinghua university emerged as aggressive acquirers of chip manufacturing capacity. One of the major targets for Chinese acquisition was the takeover of chipmaker Aixtron which operated both in Europe and the US and was blocked by both the Germans and the Americans.

There are at least three sources of tension in this complex relationship:

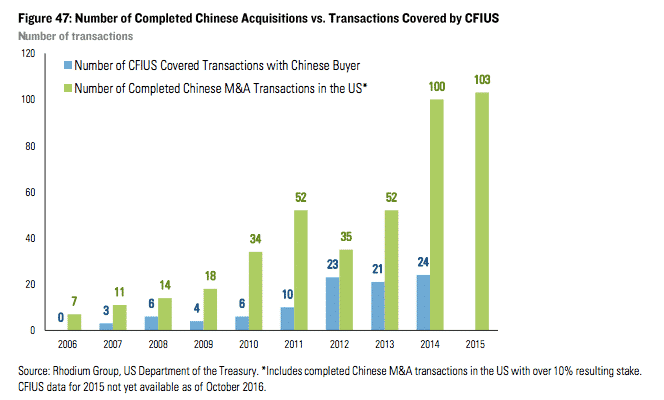

(1) the political tensions that may be caused by one sided, state-directed acquisition programs over the question of what is and what is not a “market economy”. As China has invested up the value chain it has focused its investment on the US and Germany. The US in the 1970s put in place a robust procedure for vetting foreign investments. The key agency here is the the cabinet level CFIUS, Committee on Foreign Investment in the United States, which has been busy recently:

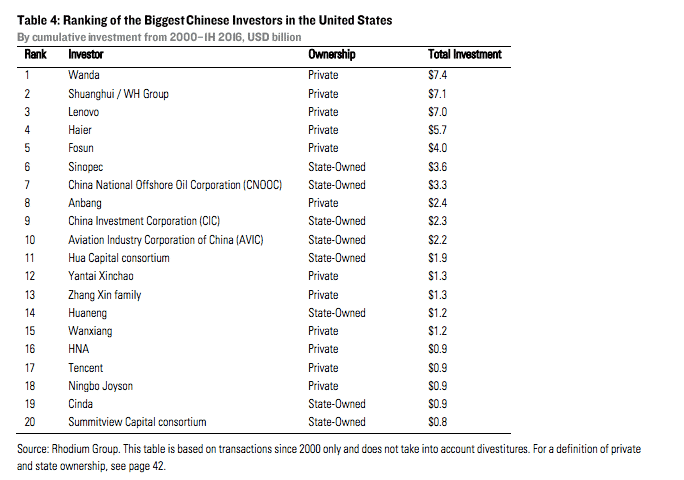

Germany has no similar provisions. Germany is caught in the awkward position of having neither national safeguards nor EU level policy. The headline deals that have raised concerns in Germany were “Midea’s acquisition of robotics maker KUKA (EUR 4.4 billion); Beijing Enterprises’ acquisition of waste incineration and power generation company EEW Energy (EUR 1.4 billion); CIC’s investment in German property group BGP (EUR 1 billion); and China National Chemical Corporation’s acquisition of industrial machinery maker KraussMaffei Group (EUR 925 million).” They are not German national champions but they are in the ranks of significant technological innovators of the second tier, which Germany regards as the secret to its enduring success in manufacturing. As Rhodium comments “… the German political and business elites continue to be highly divided whether, and if so what specific changes to the government’s traditionally open approach to foreign investment are necessary.” There is talk of a “new realism in German-Chinese economic relations.”

Tough talk of course plays well at home, but if we are in a new age of realism then we do indeed have to be realistic. The account of Gabriel’s trip to Beijing in November 2016 by Deutsche Welle’s Frank Sieren is striking:

“The German economics minister was thoughtful and rather quiet on Tuesday in Beijing. He had just found out what it means to play “tit for tat” with an 800-pound heavy gorilla. At first, his Chinese interlocutors were shocked that Germany thinks it can behave like the US. Then they made it clear to Gabriel that he was on the way to harming Sino-German relations for good. Gabriel would prefer not to, so his tone later on that day at a reception at the German embassy in Beijing was conciliatory, even full of understanding. He said that he understood that China does not want to be the factory of the world forever and that Chinese companies are already providing competition to German companies. He said that he understood that China cannot open up its markets from one day to the next because Beijing has to ensure that there will be no social upheavals. Finally, as economics minister he made it clear in relation to Chinese companies in Germany that he is not only a minister for the German economy but a minister for the economy in Germany. Nonetheless, he said that problems had to be talked about in the open.”

Indeed, Germany’s problem is that it must map its future as top dog in Europe in relation to not one but two 800 pound gorillas. The Chinese takeover of the German chip company was unpopular not just in the German media but in security policy circles in the US. As Sieren continues:

“A Chinese investment fund wanted to take over the German chip equipment maker Aixtron but Washington does not want China and Germany to join hands in this area and put up strong competition to US companies. Therefore, it was not that surprising that it seems to have just clicked with the CIA that the systems can be used for military purposes, even though since its founding in 1983 Aixtron has sold over 3,000 of them for the semi-conductor industry all over the world, including to South Korea, Taiwan and China. Without anyone in the West ever having complained in the past. But this argument did not help Gabriel. He was forced to withdraw the approval that he had given for the takeover in September.

But out of this emergency situation it seems that he has done something virtuous. So as not to appear like a lackey of the US he circulated plans in the press to push for more EU regulation of foreign investment to prevent foreign takeovers of certain technology companies unless the same rights were given to EU companies. He particularly made it clear that this should be the case if a state was behind a deal, tactfully not mentioning China. However, the fact that his plans will not be easy to implement became abundantly clear when he arrived in Beijing. It seems from his circle that Gabriel’s personal views on state involvement are different. Qatar has shares in Volkswagen but this apparently is not so bad. It is also not surprising that reactions in Brussels were mixed. EU commissioner for the digital economy Günter Oettinger even “liked” it. But he will not be dealing with this matter in future since he is going over to budget and human resources. The Commission’s message was that nothing in this direction was currently in the pipeline. Of course, nobody wants to make too much effort considering there was no united position even in the question of China’s role in the South China Sea and there is no united position on China’s status as a market economy.

Some East European EU members seem to think that Beijing is more useful to them than Brussels. Gabriel’s understanding of legal matters seems too limited for a one-man attempt. In other cases, affected companies have sued and mostly won. It does not look as if the law will be changed, which does not make it easier for him. China is an important country for the German economy. … VW makes most of its profits from the Chinese market even if it cannot be a majority shareholder in a joint venture. There is pressure from Germany therefore.”

Against the backdrop of this superheated field of corporate and geopolitical competition two further factors of a more strictly economic variety may intrude:

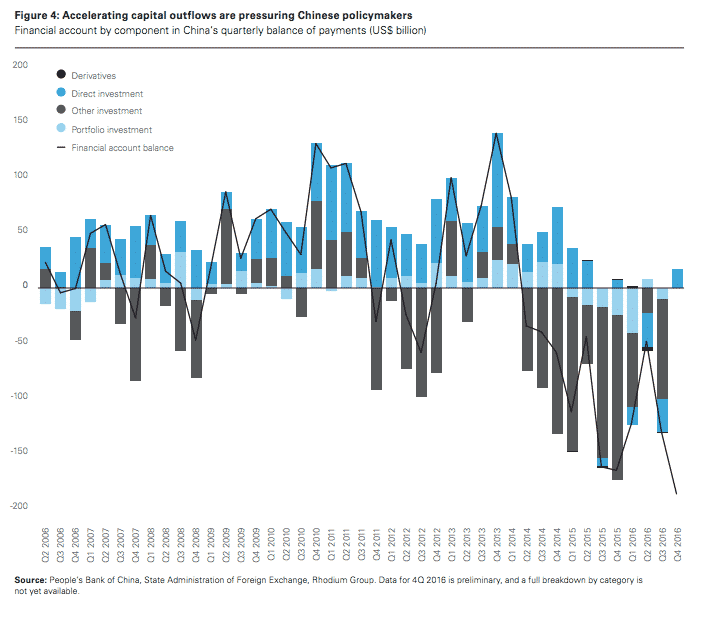

(2) the Chinese balance of payments and Beijing’s effort to manage it. The Ministry of Commerce (MOFCOM) and the National Development and Reform Commission (NDRC) vet foreign investments of more than $ 300 m and may shift the rules according to balance of payments or other pressures. If the pressure on China really builds up, Beijing may have to limit outflows. This effect should not be exaggerated since FDI is a very small element in balance of payments flows under modern conditions.

(3) More significantly, a collapse of China’s highly leveraged the level of leverage corporate debt bubble like that which struck the Japanese economy in the 1990s could bring the outward FDI surge to a halt. But that would be at the price of a major global crisis.

Takeaway 2: China’s FDI and its mixed economic regime challenges Europeans and the US to define national economic interest beyond the apparent simplicities of the “free market” paradigm.

Takeaway 3: For a second tier power as massively globally and regionally integrated as Germany is, this poses questions that are far trickier than they are for the US.

Takeaway 4: China is not the escape route to globalization that German strategists sometimes imagine, it forces Berlin straight back to the classic questions of Europe and trans-Atlantic relations.